You have submitted your mortgage application, provided your documents, and received a pre-approval. Now what? The next major step is mortgage underwriting — the most thorough review of your financial life you will ever experience. For many buyers, underwriting feels like a black box: documents go in, and eventually a decision comes out. Understanding what actually happens inside that process reduces anxiety and helps you avoid the mistakes that cause delays or denials.

This guide explains exactly what mortgage underwriters review, how long the process takes, what the possible outcomes are, and the most common reasons loans get denied — so you can keep your application on track from submission to closing.

Key Takeaways

- Underwriting is a thorough review of your income, assets, credit, and the property being purchased.

- The process typically takes 2 to 4 weeks from submission to a decision.

- Conditional approval is the most common outcome — you must satisfy specific conditions before closing.

- Respond to underwriter requests immediately — delays in documentation are the #1 cause of closing delays.

- Avoid major financial changes during underwriting: no new debt, no job changes, no large deposits.

What Is Mortgage Underwriting?

Mortgage underwriting is the process by which a lender’s underwriter evaluates the risk of lending you money to buy a specific property. The underwriter reviews your complete financial profile — income, employment, assets, credit history, and debts — alongside the property’s appraisal and title report to determine whether the loan meets the lender’s guidelines and whether you are likely to repay it.

The Four Pillars of Underwriting: The Four Cs

Underwriters evaluate mortgage applications through the lens of the Four Cs — a framework used across the lending industry.

| The Four Cs | What It Means | Key Documents Reviewed |

|---|---|---|

| Capacity | Your ability to repay — income vs. debt | Pay stubs, tax returns, W-2s, bank statements |

| Credit | Your history of repaying debts | Credit report, credit score, payment history |

| Capital | Your assets and reserves | Bank statements, investment accounts, retirement accounts |

| Collateral | The value and condition of the property | Appraisal report, title search, property inspection |

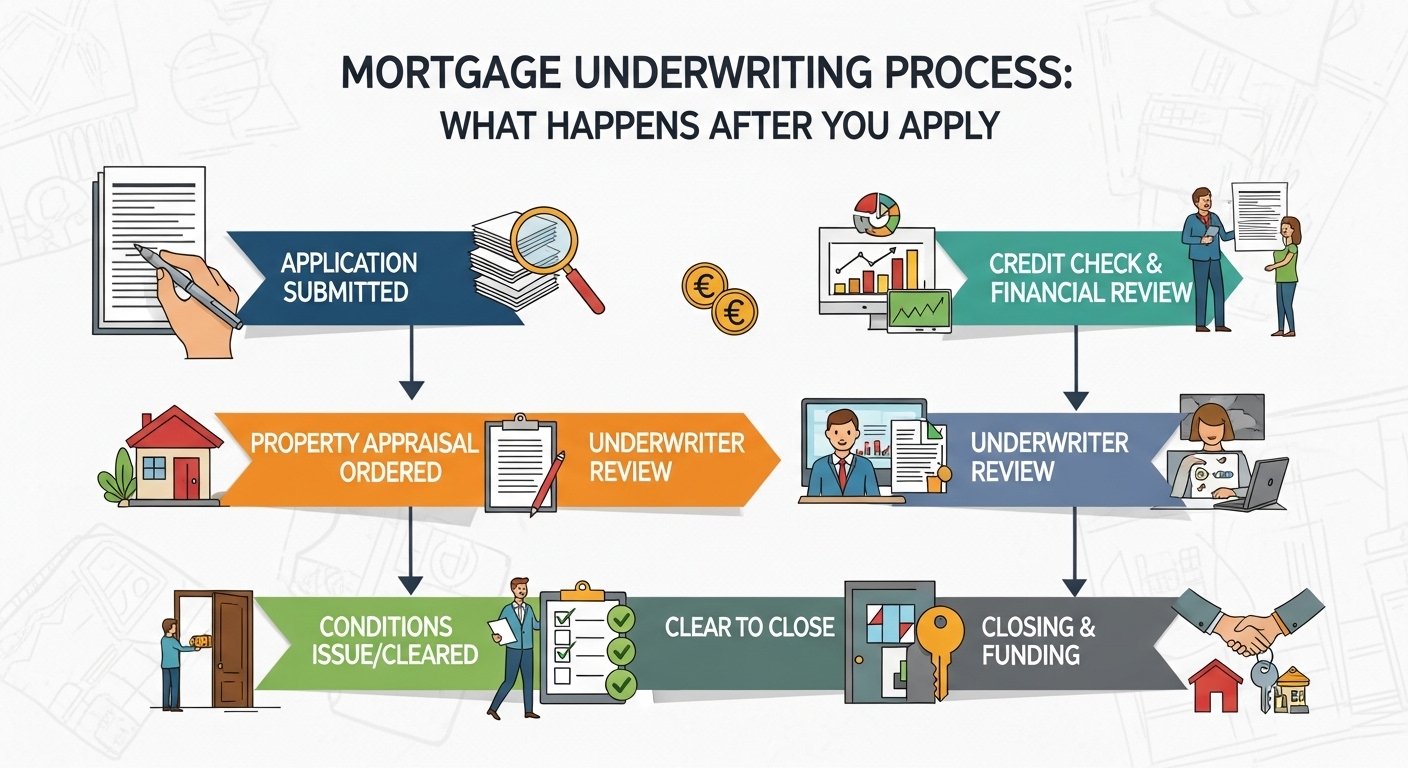

Step-by-Step: The Underwriting Process

Step 1: File Submission

Once you have a signed purchase agreement and have submitted all required documents, your loan officer submits your complete file to underwriting. The underwriter is assigned and begins their review.

Step 2: Initial Review and Conditions

The underwriter reviews your file and issues one of three decisions: approved, approved with conditions, or suspended (more information needed). Conditional approval is the most common outcome — the underwriter approves the loan subject to specific conditions that must be satisfied before closing.

Step 3: Satisfying Conditions

Common conditions include providing additional documentation, a letter of explanation for a large bank deposit, updated pay stubs, or proof of homeowners insurance. Respond to every condition as quickly as possible — delays in satisfying conditions are the leading cause of closing delays.

Step 4: Clear to Close

Once all conditions are satisfied, the underwriter issues a Clear to Close (CTC) — the final approval that allows the closing to be scheduled. You will receive your Closing Disclosure at least three business days before closing.

Common Reasons Mortgages Are Denied in Underwriting

- Income verification issues: Self-employment income, gaps in employment, or income that cannot be fully documented.

- Debt-to-income ratio too high: New debts taken on after pre-approval push DTI above the lender’s limit.

- Property appraisal comes in low: The home appraises for less than the purchase price, creating a gap the buyer must cover.

- Title issues: Liens, judgments, or ownership disputes discovered during the title search.

- Credit score drop: A new late payment or new debt application during underwriting lowers the score below the minimum.

“The number one thing buyers can do to keep underwriting on track is to respond immediately to every request and make zero financial changes until after closing. No new credit, no job changes, no large cash deposits.” — Mortgage Underwriter

What Not to Do During Underwriting

The period between application and closing is not the time to make financial moves. Underwriters re-verify your financial situation shortly before closing, and any changes can jeopardize your approval.

- Do not apply for new credit cards, car loans, or any other financing

- Do not make large cash deposits without a clear paper trail

- Do not change jobs or become self-employed

- Do not make large purchases on existing credit cards

- Do not co-sign on anyone else’s loan

FAQ

How long does mortgage underwriting take?

Mortgage underwriting typically takes 2 to 4 weeks from the time your complete file is submitted. Some lenders offer automated underwriting that can provide a decision in days, while manual underwriting for complex files can take longer. The biggest variable is how quickly you respond to requests for additional documentation — delays on your end directly extend the timeline.

What does conditional approval mean?

Conditional approval means the underwriter has reviewed your file and is prepared to approve the loan, but requires additional documentation or clarification before issuing a final approval. Common conditions include updated pay stubs, a letter of explanation for a large bank deposit, proof of homeowners insurance, or documentation of a gift fund. Once all conditions are satisfied, the underwriter issues a Clear to Close.

Can a mortgage be denied after conditional approval?

Yes, though it is uncommon. A mortgage can be denied after conditional approval if you fail to satisfy the conditions, if new information comes to light during the final verification, or if your financial situation changes materially before closing — such as losing your job, taking on new debt, or having a significant drop in your credit score. This is why it is critical to avoid any financial changes between approval and closing.

What happens if the home appraisal comes in below the purchase price?

If the appraisal comes in below the purchase price, the lender will only approve a loan based on the appraised value. You have several options: negotiate with the seller to reduce the price to the appraised value, pay the difference between the appraised value and the purchase price in cash, challenge the appraisal with a formal reconsideration of value, or walk away from the deal if your contract includes an appraisal contingency.