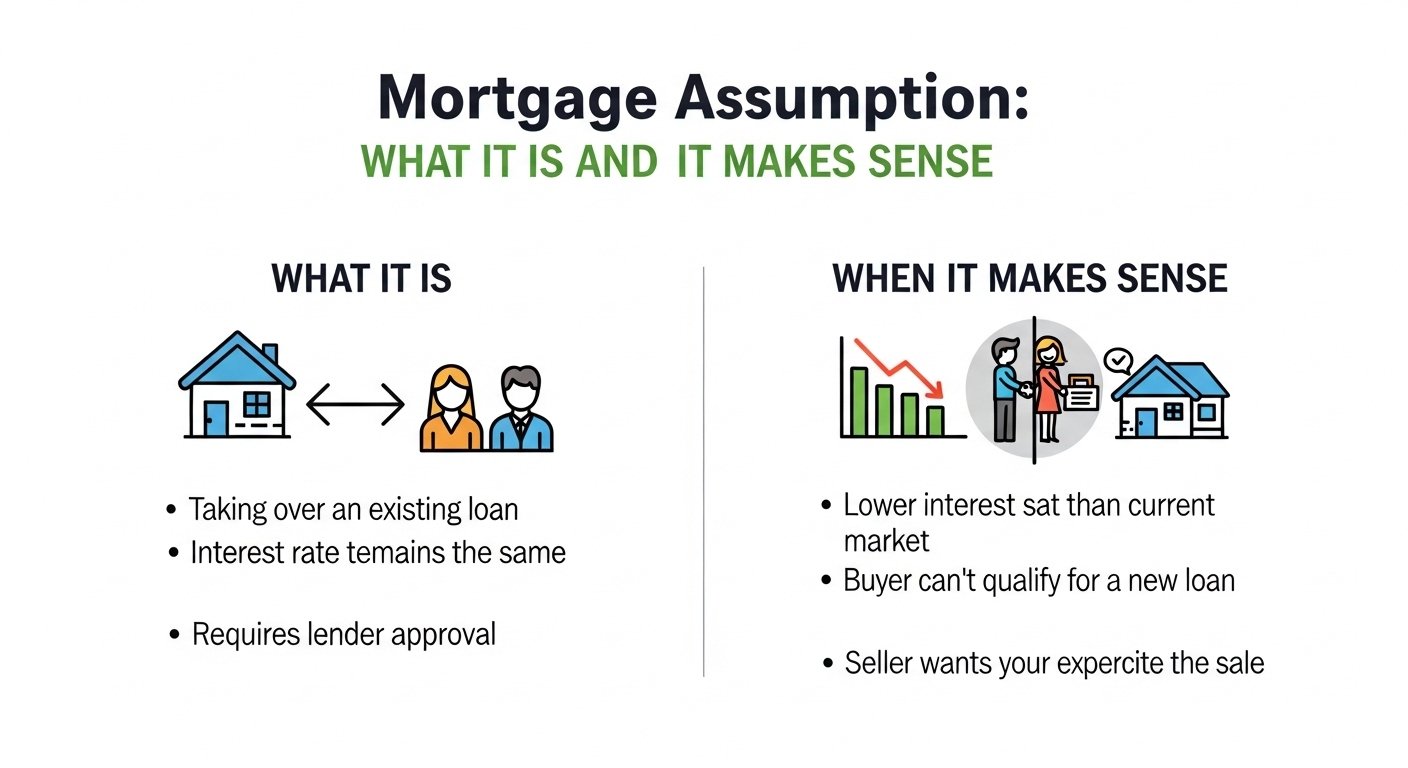

In a high-interest-rate environment, one of the most powerful — and underutilized — strategies for homebuyers is mortgage assumption. When you assume a mortgage, you take over the seller’s existing loan, including their interest rate, remaining balance, and loan terms. If the seller locked in a 3% rate in 2020 and current rates are 7%, assuming that loan could save you hundreds of dollars per month and tens of thousands over the life of the loan.

Not all mortgages are assumable, and the process has unique challenges — particularly the need to cover the gap between the seller’s loan balance and the purchase price. This guide explains exactly how mortgage assumptions work, which loans qualify, and when this strategy makes financial sense for buyers and sellers alike.

Key Takeaways

- FHA, VA, and USDA loans are assumable — conventional loans generally are not.

- The buyer must qualify with the lender and be approved to assume the loan.

- The buyer must cover the gap between the loan balance and the purchase price in cash or a second loan.

- VA loan assumptions by non-veterans can affect the seller’s VA entitlement.

- Assumption fees are typically much lower than standard closing costs.

Which Mortgages Are Assumable?

Not all mortgages can be assumed. The assumability of a loan depends on the loan type and the terms of the original mortgage agreement.

| Loan Type | Assumable? | Notes |

|---|---|---|

| FHA loans | Yes | Buyer must qualify with lender |

| VA loans | Yes | Buyer does not need to be a veteran; affects seller’s entitlement |

| USDA loans | Yes (with approval) | Buyer must meet USDA income and eligibility requirements |

| Conventional loans | Generally No | Most contain due-on-sale clauses |

| Adjustable-rate mortgages | Sometimes | Check loan documents — some ARMs are assumable |

How the Assumption Process Works

- Identify an assumable loan: Ask the seller’s agent whether the existing mortgage is assumable and request the loan details — balance, rate, remaining term.

- Apply with the lender: The buyer must apply and be approved by the existing lender. You will need to meet the lender’s credit, income, and DTI requirements.

- Cover the equity gap: The purchase price minus the loan balance must be paid in cash or financed through a second mortgage.

- Pay assumption fees: Typically $500 to $1,000 — far less than standard closing costs.

- Close on the assumption: The seller is released from the loan obligation and the buyer takes over.

The Equity Gap Challenge

The biggest practical challenge with mortgage assumptions is the equity gap. If a seller’s home is worth $450,000 and their assumable loan balance is $250,000, the buyer must come up with $200,000 in cash or financing to cover the difference. This is the primary reason assumptions are not more common — many buyers do not have the cash reserves to cover a large equity gap.

Some buyers use a second mortgage (home equity loan or HELOC from another lender) to cover the gap, though this adds a second monthly payment and a higher rate on the gap amount.

“In a high-rate environment, an assumable mortgage at 3% is worth real money. Buyers who can cover the equity gap are getting a deal that simply cannot be replicated with a new loan at current rates.” — Real Estate Attorney

VA Loan Assumption: Special Considerations

VA loans are assumable by anyone — including non-veterans — but there is an important caveat for sellers. When a non-veteran assumes a VA loan, the seller’s VA entitlement remains tied to that loan until it is fully paid off. This means the seller may not be able to use their full VA entitlement to purchase another home until the assumed loan is repaid. Sellers should consult a VA-approved lender before agreeing to a VA loan assumption by a non-veteran.

FAQ

Can I assume a conventional mortgage?

Generally no. Most conventional mortgages contain a due-on-sale clause, which requires the full loan balance to be paid when the property is sold. This effectively prevents assumption. FHA, VA, and USDA loans are the primary assumable mortgage types in the U.S. market. If you are specifically looking for an assumable loan, focus your home search on properties with these government-backed mortgages.

Do I need to qualify to assume a mortgage?

Yes. Even though you are taking over an existing loan, the lender must approve you as the new borrower. You will need to meet the lender’s credit score, income, and debt-to-income requirements — similar to applying for a new mortgage. The lender wants assurance that you can repay the loan before releasing the original borrower from liability.

What happens to the seller after a mortgage assumption?

Once the assumption is approved and closed, the seller is released from personal liability for the mortgage. The buyer becomes solely responsible for the loan. For VA loans assumed by non-veterans, the seller’s VA entitlement remains tied to the loan until it is paid off, which can limit their ability to use VA financing for a future home purchase.

How long does a mortgage assumption take?

Mortgage assumptions typically take 45 to 90 days to complete — longer than a standard purchase because the process involves the existing servicer reviewing and approving the new borrower. Some servicers are more experienced with assumptions than others, and processing times vary. Build extra time into your purchase contract timeline to account for potential delays in the assumption approval process.