Every month you make a mortgage payment, but do you know exactly where that money goes? The answer lies in mortgage amortization — the process by which your fixed monthly payment is divided between paying down the loan balance (principal) and paying the cost of borrowing (interest). Understanding amortization is one of the most powerful tools a homeowner can have.

This guide explains how mortgage amortization works, why so much of your early payments go to interest, how to read an amortization schedule, and how you can use this knowledge to pay less interest and build equity faster.

Key Takeaways

- Amortization spreads your loan repayment across equal monthly payments over the loan term.

- Early payments are mostly interest; later payments are mostly principal.

- Extra principal payments early in the loan have the greatest impact on total interest paid.

- A 15-year mortgage builds equity much faster than a 30-year mortgage.

- You can request a full amortization schedule from your lender at any time.

What Is Mortgage Amortization?

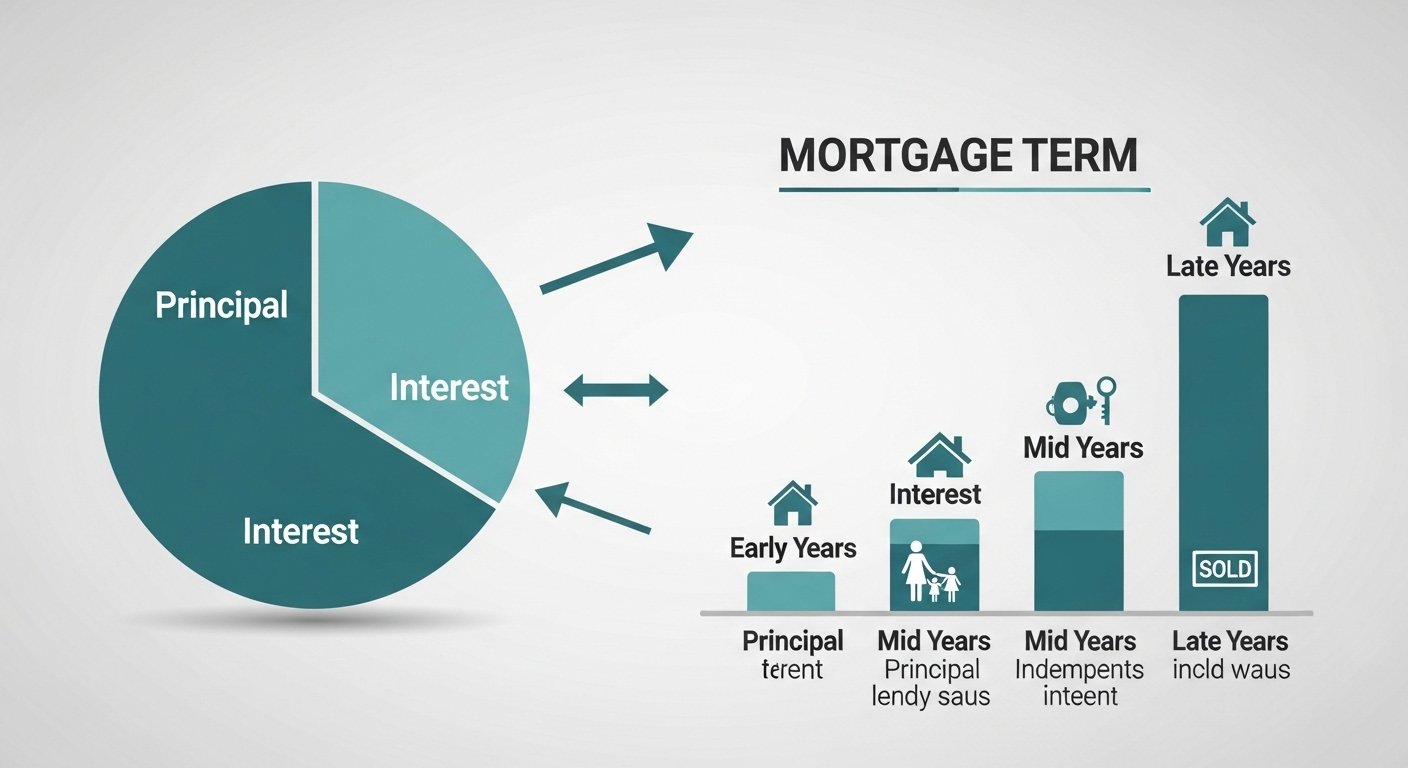

Amortization is the process of paying off a debt through regular, scheduled payments over time. With a fully amortizing mortgage, each monthly payment is the same amount, but the split between principal and interest changes with every payment. In the early years, the vast majority of each payment goes toward interest. Over time, the balance shifts until your final payments are almost entirely principal.

This front-loading of interest is not arbitrary — it is a mathematical consequence of how interest is calculated. Each month, interest is charged on the remaining loan balance. Since the balance is highest at the beginning of the loan, so is the interest charge.

Sample Amortization Schedule: $300,000 at 7% for 30 Years

Monthly payment: $1,996 (principal and interest only)

| Payment # | Payment Amount | Interest Portion | Principal Portion | Remaining Balance |

|---|---|---|---|---|

| 1 | $1,996 | $1,750 | $246 | $299,754 |

| 12 | $1,996 | $1,733 | $263 | $296,820 |

| 60 (Year 5) | $1,996 | $1,672 | $324 | $285,890 |

| 120 (Year 10) | $1,996 | $1,567 | $429 | $267,500 |

| 180 (Year 15) | $1,996 | $1,424 | $572 | $242,700 |

| 240 (Year 20) | $1,996 | $1,228 | $768 | $209,000 |

| 300 (Year 25) | $1,996 | $950 | $1,046 | $161,500 |

| 360 (Year 30) | $1,996 | $12 | $1,984 | $0 |

The Interest Front-Loading Effect

Notice in the table above that in the first payment, only $246 of the $1,996 payment reduces the loan balance. After five years of payments, you have paid nearly $120,000 — but your balance has only dropped by about $14,000. This is the reality of amortization on a 30-year mortgage, and it is why extra principal payments early in the loan are so powerful.

15-Year vs. 30-Year Amortization Comparison

| Loan: $300,000 at 7% | 30-Year Mortgage | 15-Year Mortgage |

|---|---|---|

| Monthly payment (P&I) | $1,996 | $2,696 |

| Total payments | $718,560 | $485,280 |

| Total interest paid | $418,560 | $185,280 |

| Interest savings | — | $233,280 |

| Equity after 5 years | ~$14,000 | ~$65,000 |

“Most homeowners are shocked when they see their amortization schedule for the first time. Understanding it is the first step toward making smarter decisions about extra payments and refinancing.” — Mortgage Educator

How to Use Amortization to Your Advantage

Armed with an understanding of amortization, you can make strategic decisions that save significant money. Making extra principal payments early in the loan eliminates future interest on that balance for the remaining loan term. Even $100 extra per month in the first year of a 30-year mortgage can save over $25,000 in total interest. Request your full amortization schedule from your lender and use it as a roadmap for your payoff strategy.

FAQ

Why do early mortgage payments go mostly to interest?

Interest is calculated each month on the remaining loan balance. Since the balance is at its highest at the beginning of the loan, the interest charge is also at its highest. As you pay down the principal over time, the interest portion of each payment decreases and the principal portion increases. This is the mathematical structure of amortization and applies to all fully amortizing loans.

How can I get my mortgage amortization schedule?

You can request a full amortization schedule from your lender or loan servicer at any time. Many online mortgage calculators also generate detailed amortization schedules — simply enter your loan amount, interest rate, and term. Your monthly mortgage statement may also show how much of each payment goes to principal versus interest.

Does making extra payments change my amortization schedule?

Yes. Extra principal payments reduce your loan balance faster than the standard schedule, which means less interest accrues in subsequent months. This effectively shortens your loan term and reduces total interest paid. Your monthly payment amount stays the same, but more of each future payment goes toward principal because the balance is lower. Ask your servicer to provide an updated payoff date after making significant extra payments.

What is negative amortization?

Negative amortization occurs when your monthly payment is less than the interest owed, causing the unpaid interest to be added to your loan balance. This means your balance grows over time instead of shrinking. Negative amortization was common in certain adjustable-rate mortgage products before the 2008 financial crisis and is now heavily regulated. Most standard mortgages today are fully amortizing and do not have this risk.